• Step-by-step guide to managing your roof insurance claim efficiently

• Essential documentation and negotiation tips for maximized claim potential

• Common pitfalls to avoid and expert advice for a speedy, favorable resolution

Identifying Potential Roof Damage

When it comes to your home, the roof is a formidable barrier between nature’s elements and your cherished living space. However, even the sturdiest roofs can succumb to the wrath of Connecticut’s summer storms. To prevent a small issue from ballooning into a costly headache, swift recognition of problematic signs is essential. Be vigilant for missing shingles, a telltale harbinger of underlying damage, indicative of the urgent attention your roof may require.

In the event of a storm, another less overt but equally concerning symptom to lookout for is the presence of leaks or water stains on your ceilings or walls. Water infiltration can lead to mold, rot, and a myriad of structural issues that compromise the integrity of your home. Furthermore, inspect your gutters and downspouts—as these can often become clogged with debris, causing water to back up and seep beneath your roofing material. A regular inspection routine could spell the difference between a quick fix and a large-scale insurance claim.

Yet, it’s not just about what you can see; after a storm, be sure to inspect your attic or crawl spaces for any signs of water penetration or daylight peeking through the roof boards. Document every anomaly with clear photos and detailed notes, as these records are vital when managing your roof insurance claim after damage. With a keen eye and due diligence, you can catch the early signs that scream for your roof’s rescue before they escalate beyond repair.

Understanding Your Coverage Is Key

After identifying the red flags of roof distress, it’s crucial to understand the nuances of your insurance policy. Don’t wait until after disaster strikes to familiarize yourself with the specifics of what’s covered. Knowledge is power, and in this case, it means knowing whether damage from natural wear and tear, or specific events like storms, are included under your policy. Policies differ, and so does the extent of coverage offered, so take the time to read the fine print.

Knowing the details can save you time and stress in the long run. Should a dreaded event occur, you’ll be prepared to confidently navigate the claims process with your insurer. This empowers you to make informed decisions about repairs and claim management, ensuring that you are adequately advocating for your entitlements. Remember, a well-informed homeowner stands a better chance of maximizing their claim’s potential, securing the necessary funds for a full restoration.

Initiating the Claim Process

Once your policy’s coverage is crystal clear, the next step is to promptly reach out to your insurance provider. Timeliness can’t be overstressed; insurance companies often have strict reporting deadlines post-incident. Notifying your insurer quickly not only complies with these terms but also accelerates the inspection and repair process. It’s the best way to safeguard your home against the chance of further damage, especially critical during the tempestuous summer months in Connecticut.

During your call, be concise yet thorough about the damage—a skill that becomes easier with the keen documentation you’ve conducted. The insurance company will likely schedule an inspection by an adjuster to verify your claim, a pivotal moment in the claims process. By laying the groundwork with clear communication and documentation, you set the stage for a straightforward assessment, getting you one step closer to settling your claim and starting the necessary repairs.

Step 1: Evaluate the Roof Damage

Begin by carefully assessing the extent of the damage to your roof. Look for missing shingles, leaks, or any areas that are visibly compromised. Document everything with clear photos and notes as these will be crucial for your insurance claim.

Step 2: Review Your Insurance Policy

Before filing a claim, thoroughly review your homeowner’s insurance policy to understand what is covered. Pay special attention to any clauses about roof damage and the type of incidents that are eligible for a claim, such as storm damage.

Step 3: Contact Your Insurance Company

Reach out to your insurance provider to report the damage immediately. They’ll provide instructions on the claims process and might schedule an appointment for an adjuster to inspect your roof.

Step 4: Gather Documentation

Compile all the necessary documentation required for managing your roof insurance claim after damage. This includes previous inspection reports, receipts for any repairs, photos of the damage, and your detailed notes from Step 1.

Step 5: Meet With the Insurance Adjuster

When the insurance adjuster visits, walk them through the damage you’ve documented. Your honest and detailed account will help them assess the claim accurately.

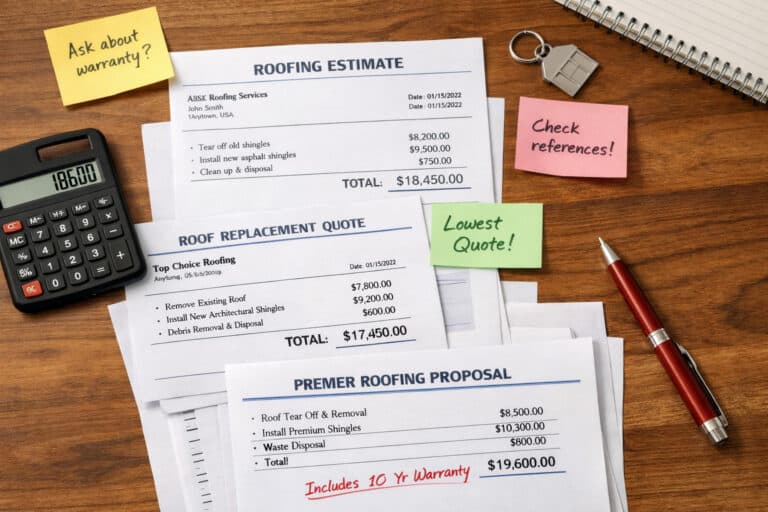

Step 6: Obtain Roof Repair Estimates

Get quotes from licensed roofing contractors in Connecticut. These estimates will be essential when discussing the claim settlement with your insurer to ensure that the compensation reflects the true repair costs.

Step 7: Negotiate Your Claim

If necessary, negotiate the claim with your insurance company, using the adjuster’s report and contractor estimates as leverage. Remember, the goal is to reach a fair settlement that covers the costs of repairing your roof correctly.

Step 8: Schedule the Repairs

Once your claim is approved, schedule the roof repairs. It’s best to get this done as soon as possible, especially during the summer months in Connecticut, to prevent further damage due to weather changes or storms.

Mistakes to Avoid When Managing Your Roof Insurance Claim

When faced with roof damage, the steps you take can greatly impact the outcome of your insurance claim. Homeowners often inadvertently commit errors that could compromise their chances of a favorable claim resolution. Being aware of common missteps is just as crucial as knowing the right steps to take.

Mistake 1: Neglecting Immediate Damage Assessment

Many homeowners delay inspecting their roof after a storm, which can lead to missed or underestimated damage. Act promptly to assess the situation — failure to do so can cause further harm and weaken your claim.

Mistake 2: Overlooking Policy Details

Overlooking the details of your insurance policy can lead to unfounded assumptions about coverage, which may result in denied claims. Always review your policy closely to understand what is specifically covered and under what conditions.

Mistake 3: Inadequate Documentation

A common pitfall is not taking enough photos or notes to accurately document the damage, leading to insufficient evidence to support your claim. Ensure that you capture all damage and keep detailed records right from the start.

Mistake 4: Poor Communication with Insurance Adjusters

Under-communicating with the insurance adjuster or providing vague details can hinder your claim’s evaluation. Be clear and thorough when presenting your case to the adjuster to facilitate an accurate damage assessment.

Mistake 5: Not Acquiring Multiple Repair Estimates

Accepting the first repair estimate can leave money on the table. Obtain multiple quotes to ensure you receive fair compensation that reflects the cost of the required repairs.

Mistake 6: Hasty Claim Negotiations

Rushing through the claim negotiation process without proper consideration or understanding can result in a less favorable outcome. Take your time to negotiate with the insurance company, guided by the adjuster’s report and repair estimates, to reach a just settlement.

Mistake 7: Delaying Repair Work

Procrastinating on scheduling the necessary roof repairs can lead to additional damage and higher costs. Once your claim is settled, prioritize the repair work, especially during the volatile summer weather in Connecticut.

Gathering Critical Documentation

When preparing to file your claim, comprehensive documentation is your best ally. It’s important to aggregate every piece of evidence that can support your case, from detailed pictures to dated notes of the damage. This collected data substantiates your claim, demonstrating the extent and impact of the roof damage to your insurer.

It’s also wise to include any relevant paperwork, such as previous inspection reports or receipts from past roof work to illustrate the pre-damage condition of your roof. Maintaining an accurate and organized record bolsters your credibility and grounds your claim negotiation in hard facts. This attention to detail reflects your due diligence and ensures none of your claim’s validity is left to question.

Meet With the Insurance Adjuster

When it’s time to meet with the insurance adjuster, your well-compiled documentation plays a critical role. Presenting clear evidence, whether it’s the aftermath of a harsh summer storm or a fallen tree limb, aids the adjuster in making a fair assessment. This step can significantly influence the success of your roof insurance claim process.

A detailed walk-through with the adjuster, pointing out the specific areas of concern, connects the dots between your documentation and the actual state of your roof. A professional evaluation from an accredited contractor may also be referenced during this visit to further substantiate your claim details. Making sure the adjuster has a complete and clear picture is crucial for a fair and expedient resolution to your insurance claim.